Background

The idea of taxing speculative financial transactions was initially proposed by the British economist John Maynard Keynes in 1936 as a mechanism to reduce uninformed short-term speculative trading and thereby reduce the excessive volatility that the financial sector caused for the real economy. Keynes was concerned that the sheer proportion of speculators could harm enterprises by becoming the dominant force in the markets for finance. The introduction of a tax on all finance transactions would be a measure to regulate this problem.

The American economist James Tobin reinvigorated the idea in 1971, after US President Nixon cancelled the US dollar’s convertibility into gold. Henceforth, other currencies became pegged to the dollar rather than to gold, and the dollar became the reserve currency for many states. Given this significant change to the global financial system, Tobin proposed taxing foreign exchange transactions, with a stronger focus on taxing international trading, and maintaining countries’ economic independence in a floating exchange rate environment. Such a tax was also aimed at reducing the opportunities for arbitrage in currency speculation.

The Asian Financial Crisis of 1997 saw a renewal of interest in the tax. An article published in Le Monde Diplomatique called for the use of revenues from a financial transaction tax to be used for global aid and development. This proposal generated an intense debate on anti-globalisation and about making the financial sector do its bit for global justice. Tobin did not oppose the use of the tax as a means of generating revenue for aid, but emphasized that this could not be the most important reason for implementing the tax.

Why is it relevant?

Since then the idea has attracted the support of latter day economic heavyweights such as Joseph Stiglitz and most recently Paul Krugman.

With such an illustrious list of advocates it does not come as a surprise that policymakers have become interested in this idea. Gordon Brown began this trend by backing an FTT at international meetings in 2009. Support has gradually grown in the European Commission, which recently published a specific proposal for a cross-EU Tobin Tax. The Commission’s draft proposes a 0.1% tax on the exchange of shares and bonds and 0.01% across derivative contracts. The tax would be levied when one of the trading partners is located within the European Union.

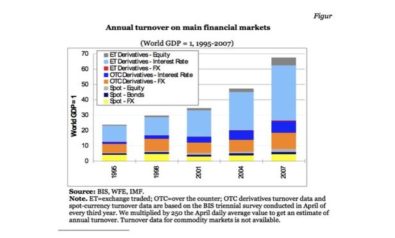

Proponents argue that it is a much-needed tax that will curb excess volatility in the global financial markets as well as bring some equity in a world where finance has a disproportionate share of global wealth. Opponents argue that it will damage the world economy, impose red tape, lower liquidity, raise the cost of capital, and end up lowering productivity and economic growth. Clearly, the Tobin tax is a powerful idea and the question the world faces is whether it is worth translating into reality.

For more than 10 years, Fair Observer has been free, fair and independent. No billionaire owns us, no advertisers control us. We are a reader-supported nonprofit. Unlike many other publications, we keep our content free for readers regardless of where they live or whether they can afford to pay. We have no paywalls and no ads.

In the post-truth era of fake news, echo chambers and filter bubbles, we publish a plurality of perspectives from around the world. Anyone can publish with us, but everyone goes through a rigorous editorial process. So, you get fact-checked, well-reasoned content instead of noise.

We publish 2,500+ voices from 90+ countries. We also conduct education and training programs on subjects ranging from digital media and journalism to writing and critical thinking. This doesn’t come cheap. Servers, editors, trainers and web developers cost money.

Please consider supporting us on a regular basis as a recurring donor or a sustaining member.

Support Fair Observer

We rely on your support for our independence, diversity and quality.

Will you support FO’s journalism?

We rely on your support for our independence, diversity and quality.